![]()

![]()

|

Unique Aspects of the

Manufacturing Industry |

|

Light Manufacturing Capabilities

One of the most common accounting software needs for inventory-based companies is “light manufacturing capabilities”. This functionality is also commonly referred to as “assembly”, “kitting”, and “bill of materials processing”. In essence the company combines multiple inventory items together to form a single inventory item for sale.

In a different example, consider the needs of a company that sells medical supplies. Such a company would most likely maintain vast shelves of medical supply items, each of which might be sold individually or as part of a kit. Typical medical supplies might include adhesive tape, gauze bandages, antibiotic cream, aspirin, thermometers, splints, blood pressure monitors, hypodermic needles, stethoscopes, stretchers, etc. These items may be priced separately or combined in various assortments to produce various first aid kits suitable for homes, businesses, recreational parks, or even emergency technicians. To build a special kit, a worker gathers the appropriate items and packs them together to create the various first aid kits. While the process of packing various medical supplies into a container is dramatically different from the assembly of a carburetor (as describe above), from an accounting perspective the system accounts for this activity in virtually the same way. As kits are completed, the system would increment the number of kits on hand by the appropriate number of units, and deplete the various components on hand by the appropriate number of units. While the kitting routine converts quantities of individual items to completed units, it is also rolls up the costs associated with each component item into the total cost of the first aid kit.

The processes we have described above are often referred to as “assembly” or “kitting”, but are also referred to as bill of materials processing, or light manufacturing. To an extent, these terms are used interchangeably throughout the accounting software industry. An understanding of this feature is extremely beneficial to manufacturing companies when it comes to using entry-level accounting systems to account for manufactured items.

At this point, many manufacturers would agree with the benefits of the assembly functionality, but would raise the issue associated with accounting for labor costs and factory worker wages. As it turns out, this is not a problem for small manufacturing companies who employ clever techniques for accounting for capturing this important information. Many entry level accounting systems allow for the establishment of a labor item in the inventory system. Once established, the labor item can be included in “assemblies” or “kits” in the same way that regular inventory items are included. To better understand this concept, consider the following example:

A customer experiences an automobile accident, and fortunately they are uninjured. They take their automobile into the shop for repair. The auto repair shop repairs the automobile, billing the customer for both time and materials used on the job (one fender $250, one bumper $350, and 8.25 repair hours at $40 each). How do they do it? Simple. The auto repair company has set up an inventory item called a repair hour which the company sells for $40 each. The company could also set up painting hours for $50 each, cleaning hours for $12.50 each, and engine steaming hours at $30 each. Many entry-level accounting systems are designed to properly accommodate these labor items which means that sales tax is not calculated on these labor items and quantities on hand are not considered in selling these items to a customer. The result is that from an accounting software perspective, the customer purchased one fender, one bumper, and 8.25 repair hours, and the customer’s sales invoice reads perfectly, complete with the appropriate sales tax calculations.

In much the same way that the auto repair shop charged the customer for labor time, manufacturers can set up labor items and then include them in the “assembly” or “kitting” process. The result is that the assembly or kitting process captures both time and materials for costing and sales pricing purposes. For example a basic first aid kit may include the following items: “Flash light ($3.00); band aides ($1.20); antiseptic spray ($2.20); ointment ($3.35); and .15 assembly hours ($1.50). In order to utilize this feature in this manner, manufacturers must identify each labor task performed during the light manufacturing process. For example, the manufacturing of a twelve dozen flags may involve 1.2 cutting hours, 2.4 sewing hours, .4 assembly hours, .1 inspection hours, and .2 packaging hours. For purposes of light manufacturing, the manufacturer would most likely use a standard length of time for each activity, even if the actual activity varied from job to job. Even the largest of organizations find it beneficial to adhere to standard times rather than actual times for the purposes of consistency and convenience.

Standard Costing Versus Actual Costs top ↑

In some cases, manufacturers may wish to track and bill the actual time incurred during the manufacturing process. This too can be accomplished with entry-level accounting systems. In order to make this happen, the manufacturer must set up the sales order as a job. For example, an order to manufacturer and deliver twelve dozen flags could be entered into the system as a job, complete with estimated costs and budgets by phase and line item. Thereafter, actual materials used in the job are depleted from inventory and introduced into the manufacturing process as part of that particular job. Similarly, time expended during the manufacturing process could be entered into the accounting system, and booked to that job. Upon completion, the accounting system’s job costing module would produce a job cost report complete with detailed listing of all materials used and all time incurred in the completion of that job. Far from being a stretch, this is exactly how many larger manufacturing organizations keep track of their “made to order” and “engineered to order” activities. In manufacturing circles, these companies are known as “Job Shop Manufacturers”.

Multiple Levels of Bills Materials

Compounding the concept of light manufacturing further is the need to include assembled items or kits in bigger items or kits. Consider, in our example above, we described the assembly of a carburetor – a process that is easily handled by entry-level accounting systems. Likewise the assembly of a front tire, rear tire, frame, and even an engine can be handled by many of today’s entry level accounting systems. A manufacturer might refer to these items as sub-assemblies. Once all of the sub-assemblies are completed, they are then assembled together to produce the final product which is a motorcycle. In order to accomplish this task, the accounting system would need to allow the manufacturer to include assembled items in other assembled items – a concept with is commonly referred to as multi-level bill of materials processing. Today, many top entry level products support this capability and the clever manufacturer can take advantage of this functionality simply by methodically breaking down the assembly process into small sub-assemblies that match the company’s manufacturing process.

Once a manufacturer has assembled an item for sale, today’s entry level products often offer the option to invoice that item with either a summary or detailed invoice. In the case of a first aid kit, the manufacturer may prefer to provide the customer with an invoice that prices the first aid kit, but lists the components of the first aid kit on the face of the invoice. In the case of a manufactured motorcycle, the manufacturer would most likely suppress the detailed list of components from the invoice, opting instead to include a single line item identifying the motorcycle.

Back Orders and Dis-Assemblies top ↑

In a perfect world, the procedures described above would all work well. However, in the real world things tend to tax your accounting system in ways that you may not perceive at first glance. For example, assume that you have five carburetors on hand, and you suddenly receive an order for 25 carburetors. In this case, you know that you are short of the necessary carburetors and that you will need to build some more units. However, you have the added complexity in that you now need your system to advise you as to the number of various carburetor components you have on hand, and the number you need to complete the order. This information is necessary to order the appropriate number of needed components from your suppliers. For example, you may have an adequate number of carburetor bowls, tubes, and springs on hand to build the necessary units, but you may be short of the necessary screws, gaskets, and housing fixtures. Rather than running out to the warehouse to hand count each component comprising a carburetor, your system needs to provide you a report detailing the needed items. While most entry-level accounting systems do not produce automatic back orders on the fly, there are work-around procedures that can accommodate the process in a pinch. For example, the manufacturer could tell the system that they have assembled the necessary 20 additional carburetors needed (even though these units have not actually been assembled). This process would force the system to deplete the various carburetor components by the appropriate amounts. Thereafter, the manufacturer could produce an inventory report which details each component of the carburetor assembly and the number of units on hand. Those units with negative balances on hand indicate the minimum number of units that must be reordered to manufacture the remaining carburetors. Once this report is prepared, the manufacturer could then dis-assemble the 20 carburetors so that the system once again reflects reality. While this process may not seem exquisite, it is a process that can and does work for thousands of manufacturers who run their businesses on entry-level accounting software products.

Along similar lines, what would happen in the event that a manufacturer suddenly sells more individual components than on-hand? For example, in our medical supply operation described above, let us assume that we have built five first aid kits and we have received an order for five rolls of adhesive tape – but our shelves are empty. In this case the manufacturer may disassemble some of the first aid kits to dig out the adhesive tape. While this process may seem arcane, in the real world situations like this do occur and when they do, your inventory system should be able to track the quantities and costs appropriately. This process would be the reverse of an assembly and would reduce quantities of first aid kits and increase the units in the individual components.

As we have learned, assemblies are a powerful

feature found in many inventory management systems. We’ve seen how job shop

manufacturers can use assembly features combined with job costing

capabilities to meet the needs of discrete manufacturer concerns. At the

other end of the spectrum is process manufacturing. In most circles, process

manufacturing is considered to be even more difficult to account for than

discrete manufacturing. This is because process manufacturing depends upon

“formulas” or “recipes” in order to complete the manufacturing process. In

our carburetor example used above, there is always one carburetor bowl used

to construct each carburetor. However in a process

With the increased use of bar code readers and scanners, it is important that items not only be identified by item number, they must also have an associated UPC/SKU code.

Issued and managed by the Uniform Code Council (UCC), a Universal Product Code (UPC) contains information identifying the manufacturer and the item in a numeric and graphical way. These codes are most often found on items sold in retail outlets.

The SKU or Stock Keeping Unit is an individual color, flavor, size, or pack of a product that requires a separate ID number to distinguish it from other items and often represents the smallest unit for which sales and stock records are maintained. Unlike the UPC code, the SKU number is assigned by the manufacturer or retailer for their own use.

To be useful, these identifiers need to be routinely stored with each inventory item so they are accessible at the time of sale and can be used for inventory tracking and control.

Multiple price levels help a manufacturer maximize the profit that he earns on each item. Prices may be determined at the time an order is placed based on negotiated terms or they may be set for specific customers.

Different prices could apply to each of the customers of a cell phone manufacturer as follows:

Imagine an order entry clerk trying to keep track of the correct pricing for the cell phone in each of the above scenarios. These examples included 6 different price points for a single item. Now add similar scenarios for every item kept in inventory and every customer. The time savings are huge for a manufacturer and virtually every business, when he can assign different price levels to inventory items and can assign a particular price level to different customers and customer types.

The best production facility in the world can not function without the materials needed for the production process. An entry level accounting package can support a manufacturer by simplifying the purchase order process which will help to assure that items are available when needed.

The first step in the procurement process is to

identify the items to order. Adequate tracking of inventory quantities on

hand, reorder points and order lead times is

What happens if you place an order for a specific item from your supplier and discover that it is not available or will have a delayed shipping date? You need to be able to find an alternate source for the item in order to meet your customer’s planned delivery date. Your inventory system can come to the rescue again when you store information about alternate suppliers for critical inventory items.

Once the items have been identified, the next step is to create a purchase order. Many manufacturers order the same materials from the same suppliers on a regular basis. Rather than having to re-enter the purchase order information each time, a more efficient approach would be to open previous purchase orders and make changes to units ordered as needed. In some systems, blanket purchase orders can be created for a single supplier, while others allow you to copy key information from one purchase order to the next. Either technique reduces the data entry time.

Many accounting software products have the ability to alert users to predefined financial conditions. With such a feature, a CFO can create simple calculations that the accounting software continuously compares against a preset value. When that value is exceeded, an alert pops on the computer screen. For example, a CFO might create calculations to sound an alert if cash on hand falls below $100,000, gross margin drops below 20% or the number of days in inventory exceeds 80. In most cases, there is no limit to the number of triggers that can be established. Using these tools properly, a manufacturer can be connected to all members of the supply chain and manage his business proactively rather than reactively. Consider a table manufacturer who knows that a tabletop coming from the teak forests of Thailand takes longer to receive than all other components. He analyzes his production process and item lead times and determines his ideal reorder point for the table tops. He would then set up a system alert to automatically e-mail his purchasing agent whenever the reorder point has been reached for these table tops. He might go a step further and e-mail the supplier directly, who could then prepare a sales order pending receipt of a completed purchase order from the purchasing agent.

Alerts or triggers could also be used to notify a customer when they are close to exceeding their credit limit so that appropriate action can be taken immediately. Again, an e-mail could be sent immediately upon entry of a customer invoice without the need for human intervention. At the same time, an e-mail could be sent to the sales team, advising them that a credit hold has been placed on the customer’s account.

Inventory Valuation Methods top ↑

An accounting system must provide numerous inventory costing options in order to meet the needs of manufacturers in different industries, in accordance with the accounting procedures they have adopted. In today’s environment, with profit margins shrinking on a daily basis, it is critical that the impact of inflation be adequately reflected in inventory costs. In industries like PC manufacturers, where costs are declining almost daily, a LIFO inventory method would result in a lower cost of goods sold, thus increasing reported profits. In other industries, where costs are increasing, the FIFO costing method would produce the lower cost of goods sold. It is important that a manufacturer have the option of choosing how to value items, so that costs are most accurately reflected.

Communication/ Visibility through the Supply Chain

From supplier to producer to customer, the more communication and coordination available, the lower the costs and the higher the net profit. What better vehicle for providing visibility throughout the supply chain than remote access via the web?

With web access, customers can check their account information, while vendors can go online to see the status of purchase orders and inventory. With this kind of immediate access, decisions can be up and down the supply chain, and rush shipments, special orders and other costly exceptions can be kept to a minimum.

Web access not only provides better communication with suppliers and customers, it will also improve communication internally as company employees gain access to accounting information from remote locations. Provided security can be fine-tuned to prohibit access to unauthorized areas of your accounting application, web delivery should be a key component of every manufacturer’s accounting solution.

With all of the focus on “just-in-time” inventory, lean manufacturing and customer satisfaction, none of this matters if there is no positive impact on the bottom line. A manufacturing company, like every other viable business, has to keep one eye firmly focused on financial information – not only the Income Statement and Balance Sheets but also critical indicators like receivables aging, working capital ratios and inventory turnover.

In order for these indicators to be useful, they

must

be available real time and accessible from any location via the Internet.

What’s more, access to

Let’s say we hire a manager to focus on improving customer service for our medical supply company. He would do everything in his power to fulfill orders on time and with quality materials. The trade off would be that he would spare no expense to meet a promised delivery date – he would generate rush orders for missing inventory, authorize staff to work overtime, and buy top quality materials so that there is no risk of customer dissatisfaction. If the company improves customer service by a factor of 10 but reduces margins by 50%, we are no better off. Rather, every initiative and operational improvement should directly impact financial results.

At a minimum the following key business indicators should be available to a small business at all times:

A company’s cash position (cash on hand plus expected collections minus expected payments) is one measure that every small business owner should be following on a daily basis.

While inventory is one critical component of cost management and therefore profitability in a manufacturing environment, it also has an immediate impact on cash flow. If sufficient quantities of critical manufacturing components are routinely unavailable, one of two situations will result – sales will decline due to delays in customer service or profitability will decline as rush orders are placed for missing components. Both of these scenarios will impact both profitability and cash flow. Monitoring the cash position of a manufacturing organization on a frequent basis is therefore a good way to determine if inventory is being effectively managed.

This ratio,

computed by dividing cost of sales by inventory value, tells you when

quantities of inventory on hand are excessive. Businesses that have low

gross profit rates should show high inventory turnover rates in order to

operate profitably. An inventory turnover ratio of .5, for example would

indicate that twice as much inventory is sitting on the shelf as has been

sold for the year. Days Receivable is the time it takes on average to collect payment on invoices. The calculation equals the total balance in accounts receivable times 365 days divided by the annual revenue. The lower the number of days, the better the company is in collecting its sales in cash.

|

|

|

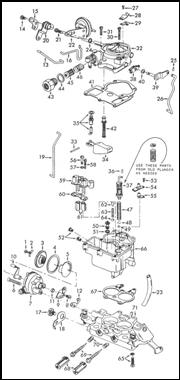

For

example, consider the needs of a company that builds and sells carburetors.

A single carburetor consists of many items as shown in figure 1. These

individual items are referred to as components and would typically include

items such as a carburetor bowl, two 4 gauge springs, 16 1/8th

inch machine screws, 4 rubber hoses, etc. An accounting system that supports

light manufacturing would allow the company to establish inventory item IDs

for each of these components, as well as the completed item – the

carburetor. In this manner, the accounting system allows the company to

track all inventory on hand. As carburetors are assembled by workers, they

simply indicate those assemblies as they occur with a quick entry to the

system, and the accounting system would automatically increment the number

of carburetors on hand by the number of built units, and would also deplete

the appropriate number of components used in the assembly. For example, if 4

carburetors were assembled on Monday morning, the system would increment the

number of carburetors on hand by 4, and deplete the number of carburetor

bowls, springs, screws, and hoses on hand by 4, 8, 64, and 16 respectively.

In this example, the worker has assembled an item using other inventory

items, and in this case, the term “assembly” is typically used to refer to

this process.

For

example, consider the needs of a company that builds and sells carburetors.

A single carburetor consists of many items as shown in figure 1. These

individual items are referred to as components and would typically include

items such as a carburetor bowl, two 4 gauge springs, 16 1/8th

inch machine screws, 4 rubber hoses, etc. An accounting system that supports

light manufacturing would allow the company to establish inventory item IDs

for each of these components, as well as the completed item – the

carburetor. In this manner, the accounting system allows the company to

track all inventory on hand. As carburetors are assembled by workers, they

simply indicate those assemblies as they occur with a quick entry to the

system, and the accounting system would automatically increment the number

of carburetors on hand by the number of built units, and would also deplete

the appropriate number of components used in the assembly. For example, if 4

carburetors were assembled on Monday morning, the system would increment the

number of carburetors on hand by 4, and deplete the number of carburetor

bowls, springs, screws, and hoses on hand by 4, 8, 64, and 16 respectively.

In this example, the worker has assembled an item using other inventory

items, and in this case, the term “assembly” is typically used to refer to

this process.

manufacturing environment, the amount of potatoes used to make potato salad

will fluctuate depending upon the amount of potato salad being produced. In

fact, all of the ingredients will fluctuate depending upon the total amount

being produced. This added complexity makes process manufacturing more

difficult to account for. Still, small manufacturers use entry-level

accounting systems to do just that. By using the “assembly” and “job

costing” and “time and billing” concepts described above, they are able to

build recipes as assembled items – and then adjust those items by building

fractions of assembled items. In this case, rather than using English

measurements such as pints, quarts, gallons, and pounds, this process is far

easier when the metric system is used to account for quantities on hand. In

this manner adjusting the total quantity of item to be manufactured, is as

simple as moving the decimal point (ie: 100 liters, instead of 1,000

liters). This process automatically adjusts the components needed by the

appropriate amounts and process manufacturing is more easily accomplished in

an entry level environment.

manufacturing environment, the amount of potatoes used to make potato salad

will fluctuate depending upon the amount of potato salad being produced. In

fact, all of the ingredients will fluctuate depending upon the total amount

being produced. This added complexity makes process manufacturing more

difficult to account for. Still, small manufacturers use entry-level

accounting systems to do just that. By using the “assembly” and “job

costing” and “time and billing” concepts described above, they are able to

build recipes as assembled items – and then adjust those items by building

fractions of assembled items. In this case, rather than using English

measurements such as pints, quarts, gallons, and pounds, this process is far

easier when the metric system is used to account for quantities on hand. In

this manner adjusting the total quantity of item to be manufactured, is as

simple as moving the decimal point (ie: 100 liters, instead of 1,000

liters). This process automatically adjusts the components needed by the

appropriate amounts and process manufacturing is more easily accomplished in

an entry level environment.  mandatory

for deciding which items to order. In addition, you should be able to

quickly determine the number units on

hand (items in stock) as well as the units available for sale (defined as

the items in stock plus items on purchase

orders less items on sales orders). This

information should be stored for each inventory item and available both in

printed reports and for export to Excel.

mandatory

for deciding which items to order. In addition, you should be able to

quickly determine the number units on

hand (items in stock) as well as the units available for sale (defined as

the items in stock plus items on purchase

orders less items on sales orders). This

information should be stored for each inventory item and available both in

printed reports and for export to Excel.  bottom line results is not enough; a business manager should be able to

examine the details supporting key indicators with the push of a button. If

information is hard to find or requires too much effort on the part of a

manager, it will not be used.

bottom line results is not enough; a business manager should be able to

examine the details supporting key indicators with the push of a button. If

information is hard to find or requires too much effort on the part of a

manager, it will not be used.